Try a free course now

Want to see if our CPD works for you? Try a free verifiable CPD course now.

Get started- 0 learners

- 0 countries

- 0 CPD resources

- 0% online

Why accountingcpd?

At accountingcpd we help accountants grow by providing high quality CPD, that will genuinely make a difference to you in your career.

Whether you want to keep up to date with the latest changes and trends, develop new skills, or prepare yourself for the next job, accountingcpd has what you need to succeed.

Huge range

Over 1,500 CPD resources to choose from. Keep up to date AND develop your professional skills with courses on a wide range of topics.

CPD Certification

Approved by leading accounting bodies, keep and download your CPD certificates on your personal CPD dashboard. Audit proof and stored securely.

Flexibility

Learn what you want, when and where you want to. From 15-minute CPD Bites, 4-hour courses, to longer-form structured diplomas and qualifications.

Partner approved

We work with leading professional bodies and expert authors to ensure you stay up to date and are able to embrace the future of our profession.

Offers

Courses

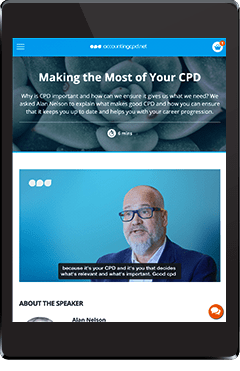

Auditing: Forming an Opinion

One of the most important parts of the auditing process is the final opinion issued on the financial statements. Sometimes, that's all that stakeholders need to see. However, providing an opinion may not be straightforward. This course guides you through the process of forming an opinion.

Read moreAI for Accountants

Are you ready to embrace the future of accounting with AI? Artificial intelligence is beginning to reshape how accountants strategise, predict, and advise. This course will help you to get to grips with the growth of AI and what it means for the profession, and to develop the tools you need to use AI effectively.

Read moreThe Trusted Business Advisor

These days your clients are looking for more from their accountants, they want a trusted business advisor. This course looks at the processes, steps and technology that enable you to understand your clients' businesses, build stronger relationships and add real value.

Read moreEthics in the Workplace

In a world full of grey areas and thorny dilemmas, acting ethically is far from straightforward. This course explores the concept of ethics and issues faced in the workplace. Discover how to adjust your own behaviour and promote ethical practices.

Read moreBuilding a Spreadsheet Forecasting Model

This course explains how to build and operate spreadsheets for forecasting, planning and business models. It's a practical guide, which takes a step-by-step approach to building, utilising and maintaining models.

Read more2023-24 Update: The Year in Accountancy

The world of accountancy is constantly changing due to new technology, evolving market requirements, and regulatory changes. So, how can you keep up and adapt? This course reviews the key headlines, developments and trends of the past year, to help you understand the implications for the profession, and plan your response.

Read more2023-24 Update: Australian Tax, Financial Reporting and Legislation

This course covers key developments across tax, superannuation, financial reporting, anti-money laundering and more, It will ensure you give your clients the latest advice on the issues important to them.

Read moreCritical Thinking for Accountants

Critical thinking is becoming increasingly important for accountants, as businesses look to you to provide insight, analysis and proposals to improve your, or your clients� business. This course explores critical thinking techniques and provides practical advice on how to use them to benefit the organisations you work with.

Read more2023-24 Update: UK & Ireland GAAP

Discover the FRC's proposed changes to UK and Ireland GAAP with this course. You'll explore common deficiencies found in financial statements, as well as the reporting requirements for foreign currency transactions and events after the end of the reporting period.

Read moreMaking Monthly Reports Worth Reading

World class finance functions produce monthly reports that managers actually read. This course enables you to delight your audience by setting clear objectives, creating compelling visuals and creating monthly reports that drive business improvement.

Read more2024 Spring Update: UK Tax

This course provides comprehensive tax updates for the first three months of this year including recent legislation, consultations, tax cases and changes, along with an expert analysis of the main announcements made in the Spring Budget on March 6th.

Read more2023-24 Update: UK Tax

Staying up to date with tax changes is vital for finance professionals. This year's UK tax updates course focuses on changes in tax for the new financial year, legislation from Finance Act 2023, announcements made in the Spring Budget, and the contents of the recent Spring Finance Bill.

Read more2023-24 Update: Excel

Microsoft issues new features for Excel all the time, but are you making the most of them? This course delivers the latest Excel updates to help you work more effectively and efficiently, with practical downloadable spreadsheets in each module.

Read moreProfessional Scepticism

This course provides guidance on developing an attitude of professional scepticism with examples demonstrating the significance of judgement in financial accounting. Discover why being sceptical is described by the IAASB as the personal and professional responsibility of every accountant.

Read moreThe ICAEW Code of Ethics

All accountants, ICAEW member or otherwise, have a public duty to remain ethical. This course explains why integrity and independence are essential for accountants and how to uphold them throughout your work.

Read moreDeveloping CFO Behaviours

This course will take you beyond the basics of being a CFO and allow you to embody the leadership role. You will build your interpersonal skills so that you can positively influence your team and develop the behaviours of a well-respected leader. Begin today to develop a clearer vision for your career.

Read moreMeasuring and Managing Your Carbon Performance

Consumers, employees and major investors are increasingly choosing climate friendly brands. This course explains how a rigorous approach to carbon performance management will enable you to measure your organisation's carbon emissions and understand how to manage and reduce your carbon footprint.

Read moreFuture of Finance: Digital Innovation

When looking towards the future of finance, it's important to understand the role of emerging digital innovations. This course explores the changing technological landscape and the specific innovations that are transforming the role of the accountant and the processes you use.

Read moreProject Management for Accountants

As an accountant you will already manage projects. But by helping you understand professional project management tools and techniques, this course will take your project management skills to the next level.

Read moreData Analysis for Accountants: Power BI

This course introduces you to Power BI, Microsoft's powerful data analysis tool, and how it can benefit you in your finance role. Transform the way you handle and analyse data, and create a range of interactive data visualisations.

Read moreDue Diligence in Buying and Selling a Business

This course explores the process of due diligence from both the buyer and the seller's perspective. You will learn the importance of due diligence for both parties and will consider the risks involved in buying or selling a business, and what you can do to minimise these.

Read moreBecoming a Diversity and Inclusion Champion

A diverse, equal, and inclusive workplace is something that employees want and employers benefit from. This course looks at equality, diversity and inclusion broadly, and offers practical ways that you can promote a healthy and happy work environment.

Read moreInsolvency for Accountants

Economic turbulence and cash flow pressures continue to drive the insolvency landscape, and accountants are increasingly playing a key role. This course enables you to spot signs of business failure and equips you to help with turnaround, and understand your role, if the insolvency process is necessary.

Read moreExcel Productivity Booster

It's easy to find yourself using Excel the same way for years at a time. This course concentrates on a range of practical and simple techniques that can make spreadsheets quicker to set up, easier for the user to use, more automated, and guard against career-threatening errors.

Read moreThe Finance Business Partner

As a finance business partner, you need credibility and influence within the management team. This course looks at the finance business partner role, and how you can develop to take on this strategic role in your or you clients' businesses.

Read more2024-25 Update: UK and Irish GAAP

Following the publication of FRED 82, the FRC has now confirmed the final changes being made to the UK and Ireland GAAP. This course provides a well-timed review of areas in the spotlight, particularly focusing on leasing transactions and revenue recognition.

Read moreData Analysis for Accountants: Getting Started

As a finance professional you use Excel to analyse data, but how often do you overlook Excel's useful features? This course looks at basic and advanced features of Excel's PivotTable tool as well as PowerPivot and Data Analysis Expressions (DAX).

Read more