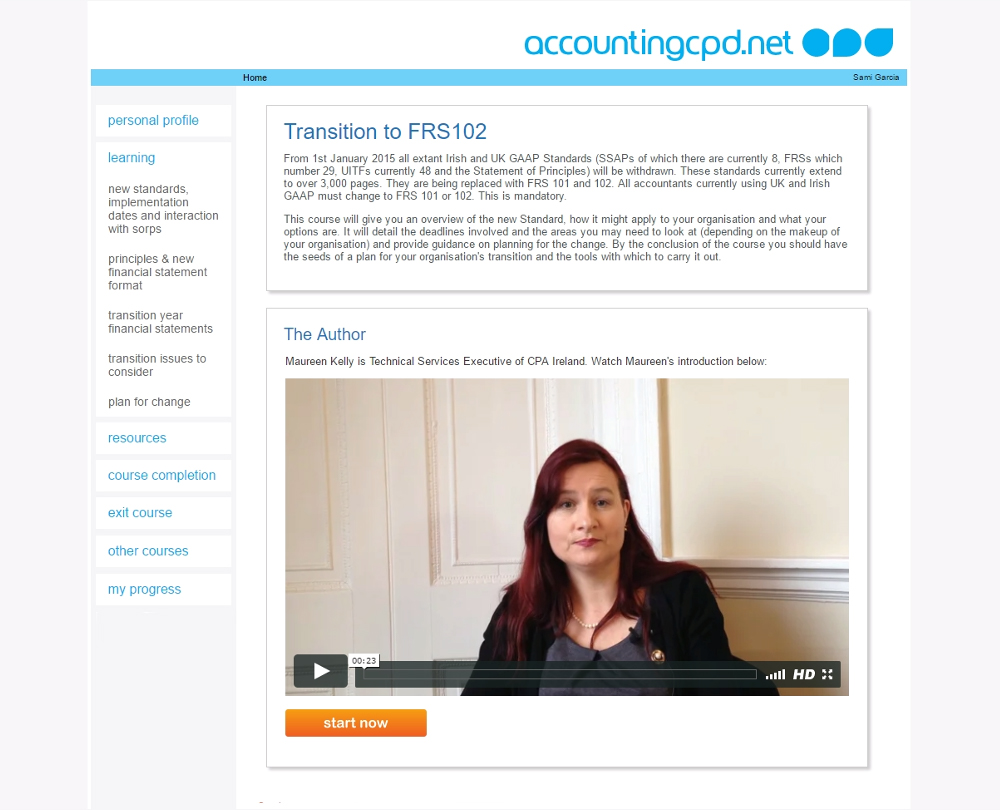

Transition to FRS102

From 1st January 2015 all extant Irish and UK GAAP Standards will be replaced with FRS 101 and 102.This course will give you an overview of the new Standard, how it might apply to your organisation and what your options are. It will detail the deadlines involved and the areas you may need to look at and provide guidance on planning for the change.

This course will enable you to

- Understand the new UK and Irish GAAP

- Recognise how the new Reporting Standards will apply to your organisation

- Understand what options are available to your organisation when it comes to adopting FRS 102

- Put a plan in place for your organisation for a smooth transition to FRS 102

About the course

From 1st January 2015 all extant Irish and UK GAAP Standards (SSAPs of which there are currently 8, FRSs which number 29, UITFs currently 48 and the Statement of Principles) will be withdrawn. These standards currently extend to over 3,000 pages. They are being replaced with FRS 101 and 102. All accountants currently using UK and Irish GAAP must change to FRS 101 or 102. This is mandatory.

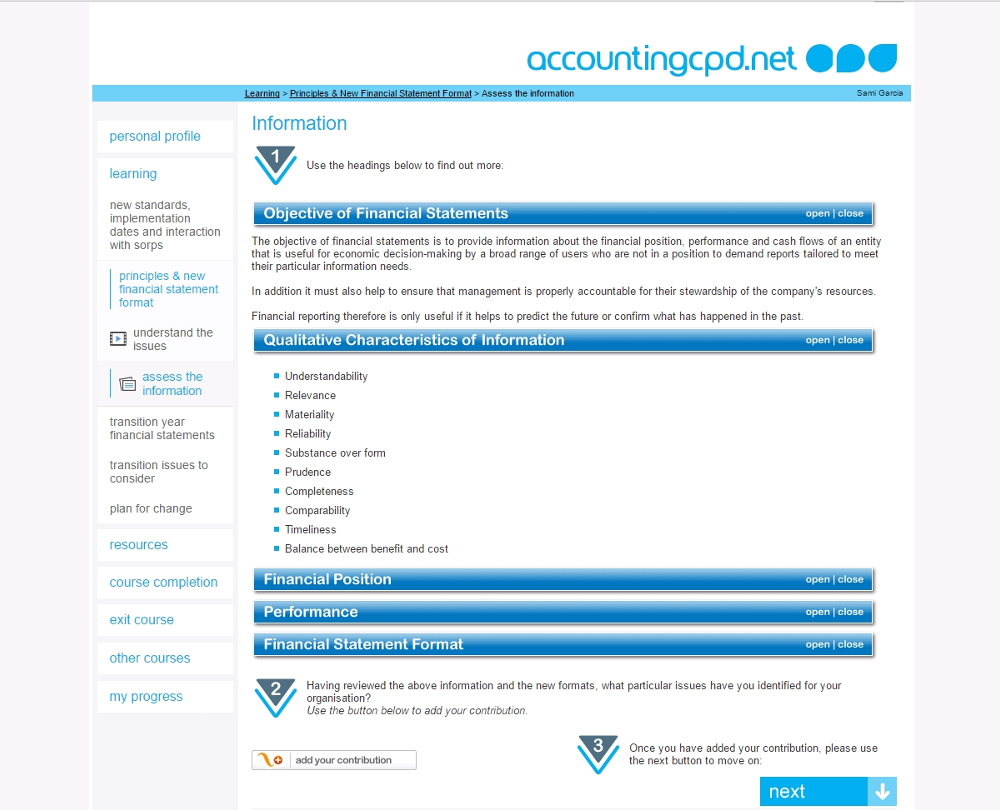

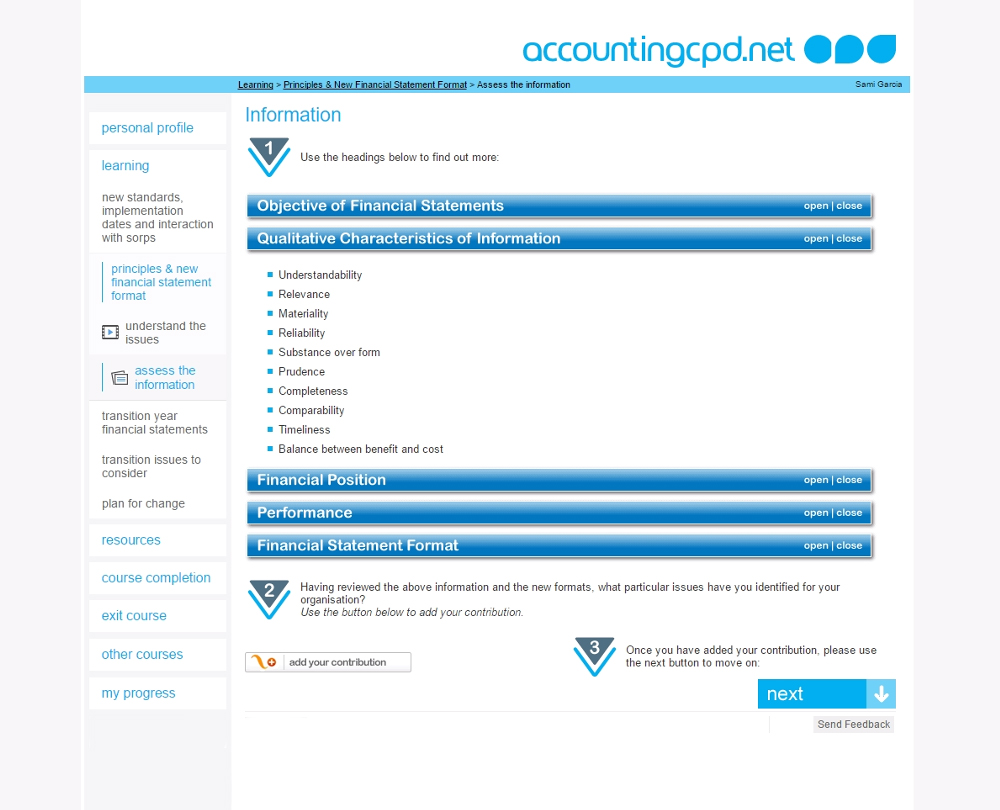

This course will give you an overview of the new Standard, how it might apply to your organisation and what your options are. It will detail the deadlines involved and the areas you may need to look at (depending on the makeup of your organisation) and provide guidance on planning for the change. By the conclusion of the course you should have the seeds of a plan for your organisation's transition and the tools with which to carry it out.

Look inside

Contents

How it works

Author

Reviews

You might also like

Take a look at some of our bestselling courses