Professional Scepticism

This course explores some of the common areas where judgement is necessary in financial decisions, and considers the appropriate response.

This course is not currently available

This course will enable you to

- Understand how professional scepticism is linked to judgement in financial reporting

- Successfully demonstrate professional scepticism at an appropriate level

- Use professional scepticism to account for non-financial assets and liabilities

- Apply professional scepticism in relation to fraud and other financial irregularity

About the course

With the increased use of judgement in financial reporting in recent years, the ability to exercise professional scepticism is an increasingly important competency for accountants.

So, what does "professional scepticism" actually mean? And, more importantly, how confident are you in exercising this all-important accounting skill? This course explores some of the common areas where judgement is necessary in financial decisions, and considers the appropriate response.

The course not only helps you exercise professional scepticism but also shows you how to demonstrate it, and ultimately make professional scepticism part of your organisation's culture.

Look inside

Contents

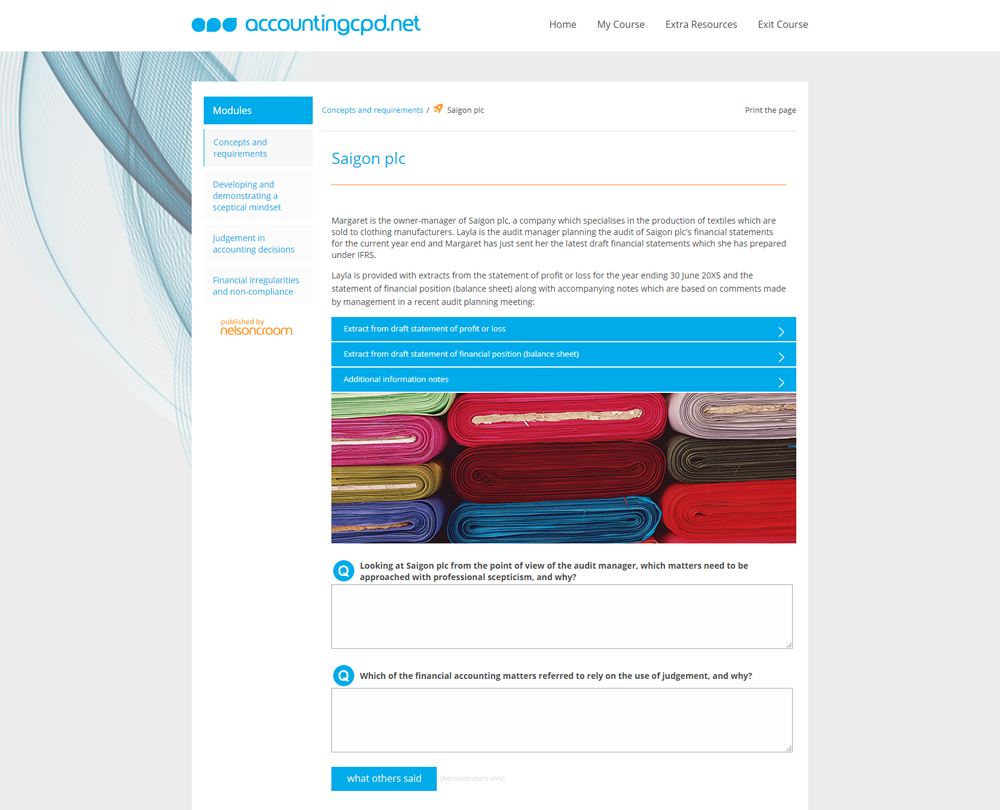

- Concepts and requirements

- What is meant by the terms professional scepticism and professional judgement?

- How is professional scepticism linked to judgement in financial reporting?

- Why is professional scepticism a focus of the professional and regulatory bodies?

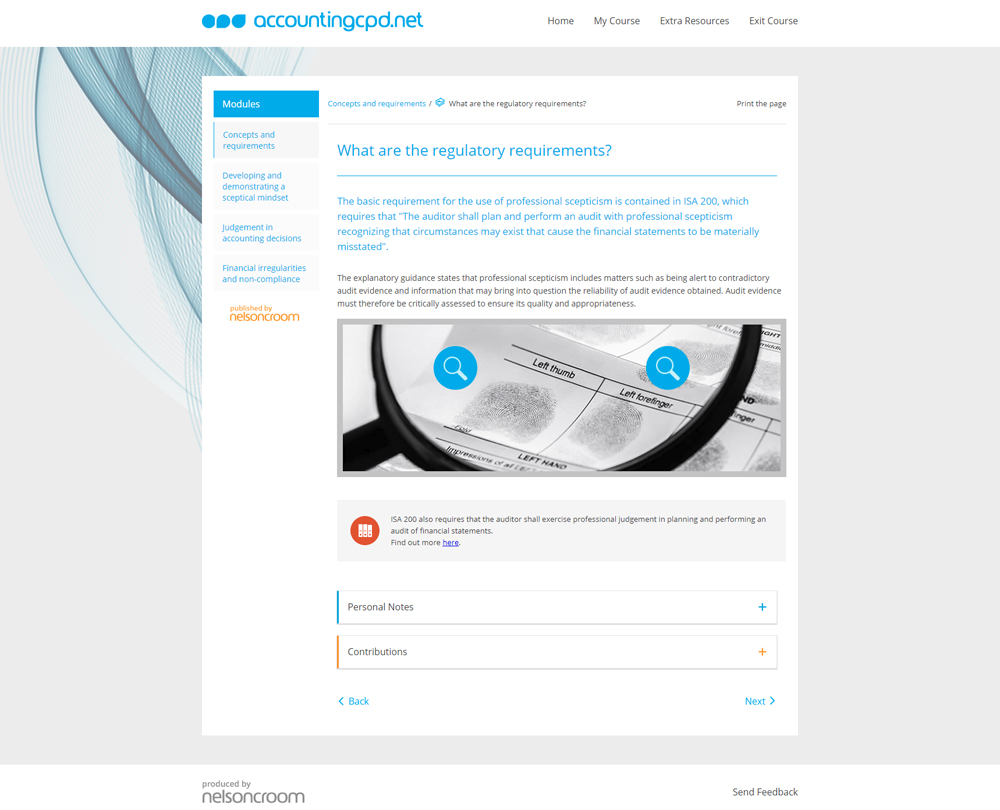

- What are the regulatory requirements?

- Developing and demonstrating a sceptical mindset

- How is professional scepticism linked to audit quality?

- How can professional firms plan to enhance professional scepticism amongst their staff?

- How can the application of professional scepticism be demonstrated?

- What is the relationship between auditor independence and professional scepticism?

- Judgement in accounting decisions

- How do I account for non-financial assets and liabilities?

- What difficulties are involved in accounting for financial instruments?

- What scepticism is involved around the impairment of assets?

- What judgement is required in the assessment of going concern?

- What guidance is given on the assessment of going concern in difficult circumstances?

- Financial irregularities and non-compliance

- What types of irregularities might I have to deal with?

- How is scepticism applied in relation to fraud and other financial irregularity?

- How is professional scepticism applied when fraud is discovered?

- What if there's a breach of law and regulations?

- What is fraudulent financial reporting?

How it works

Author

Reviews

You might also like

Take a look at some of our bestselling courses

This course is not currently available. To find out more, please get in touch.