Managing Your Transition to IFRS

This course has been revised and is up to date for 2019-20. Learn everything you need to know about these important standards, the benefits and the implications of using them, and how to make the transition a smooth one.

This course will enable you to

- Understand why the change to IFRS is happening

- Know the reporting requirements for small and medium-sized companies

- Consider the costs of the transition

- Plan a transition from financial reporting to IFRS

- Understand the non-financial implications of switching to IFRS

About the course

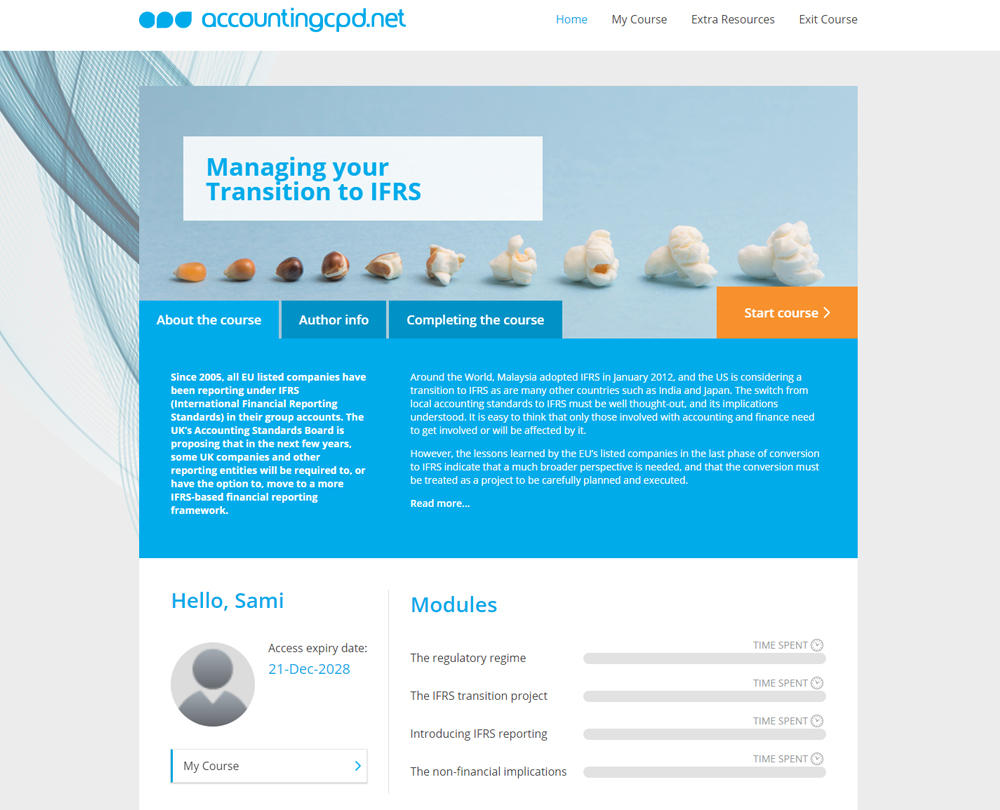

Since 2005 all EU listed companies have been reporting under IFRS (International Financial Reporting Standards) in their group accounts. In the UK, the Accounting Council (and its predecessor, The Accounting Standards Board) have developed a new financial reporting framework based on the International Financial Reporting Standards (IFRS) framework for all but the very smallest companies in the UK and Republic of Ireland. The US continues to consider a transition to IFRS, as are many other countries such as India and Japan.

The switch from local accounting standards to IFRS must be well thought-out, and its implications understood. It is easy to think that only those involved with accounting and finance need to get involved or will be affected by it. However, the lessons learned by the EU�s listed companies in the last phase of conversion to IFRS indicate that a much broader perspective is needed, and that the conversion must be treated as a project to be carefully planned and executed.

Look inside

Contents

- The regulatory regime

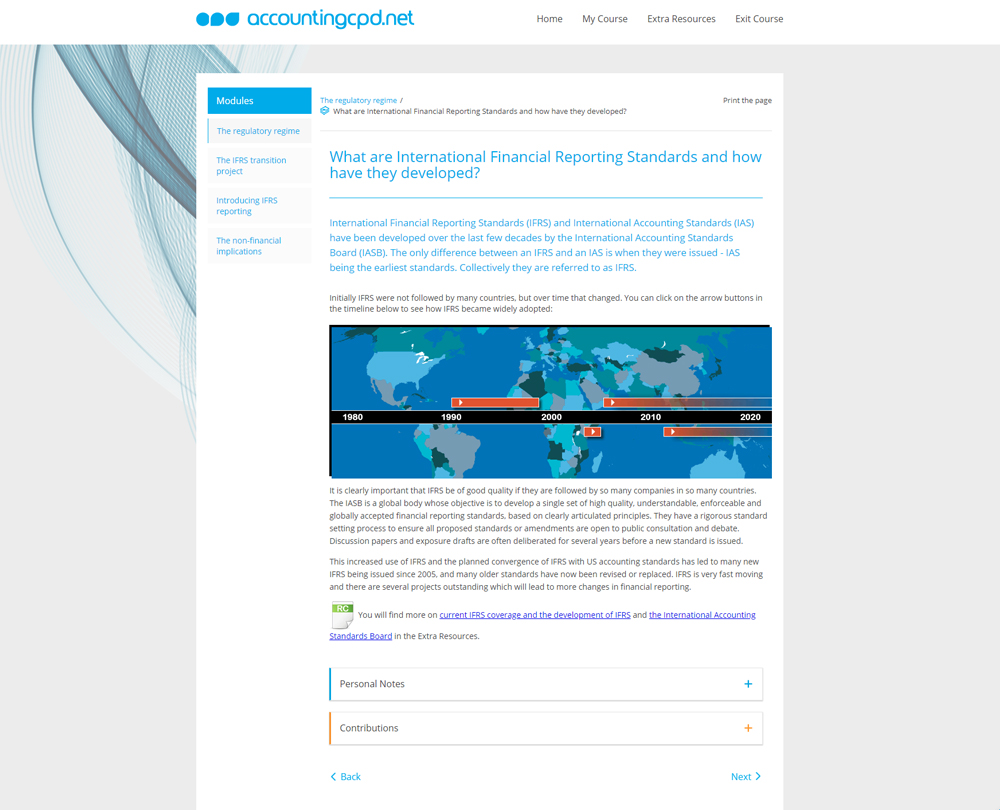

- What are International Financial Reporting Standards and how have they developed?

- Why are countries and companies switching to IFRS?

- What are the reporting requirements for small and medium sized companies?

- The IFRS transition project

- What are the benefits of establishing an IFRS transition project?

- What should be the main stages in planning the project?

- What is the cost of IFRS transition?

- What role can external advisors play in the project?

- Introducing IFRS reporting

- How can the main accounting impacts be identified?

- Will there be any effect on presentation and disclosure requirements?

- What systems and controls issues need to be considered?

- How can I make sure that IFRS is embedded in the organisation?

- The non-financial implications

- What are the implications for employees, suppliers, customers etc?

- Will the transition have any effects on company strategy, policies and regulation?

- What effects will the transition have on the users of my financial statements?

- How can transition issues be effectively communicated to those outside the company?

How it works

Author

Reviews

You might also like

Take a look at some of our bestselling courses