Business Asset Disposal Relief

This course, formerly known as Entrepreneurs' Tax Relief has been revised and is up to date for 2021/22. This course looks at how this important tax relief is applied and the requirements necessary for an individual trader, partner, trustee or shareholder to qualify.

This course will enable you to

- Advise on how to benefit from a reduced rate of tax when selling a business

- Incorporate businesses or reorganise companies, whilst claiming or preserving relief

- Advise partners in a business who are selling their interest

- Know how to expand or make investments without losing relief

- Understand the rules around retirement

- Understand how to grant employees share options and still qualify for relief on subsequent disposals

About the course

Business Asset Disposal Relief reduces the tax payable on the sale on some or all of a business by someone who has shares in it or did so when it ceased. If all the conditions are met, you or your client will be eligible for tax relief, but what are those conditions and how can you be sure you're getting the reliefs that you or your clients are due?

The course will explain how the relief is applied and all the requirements necessary for an individual trader, partner, trustee or shareholder to qualify. It will cover planning opportunities and pitfalls and how the relief applies in certain circumstances, in particular, where other reliefs are involved.

This course, formerly known as Entrepreneurs’ Tax Relief has been revised and is up to date for 2021/22

Look inside

Contents

- Application, calculation and claims

- What types of disposals are eligible for relief?

- How is relief calculated and claimed?

- How are other capital losses taken into account?

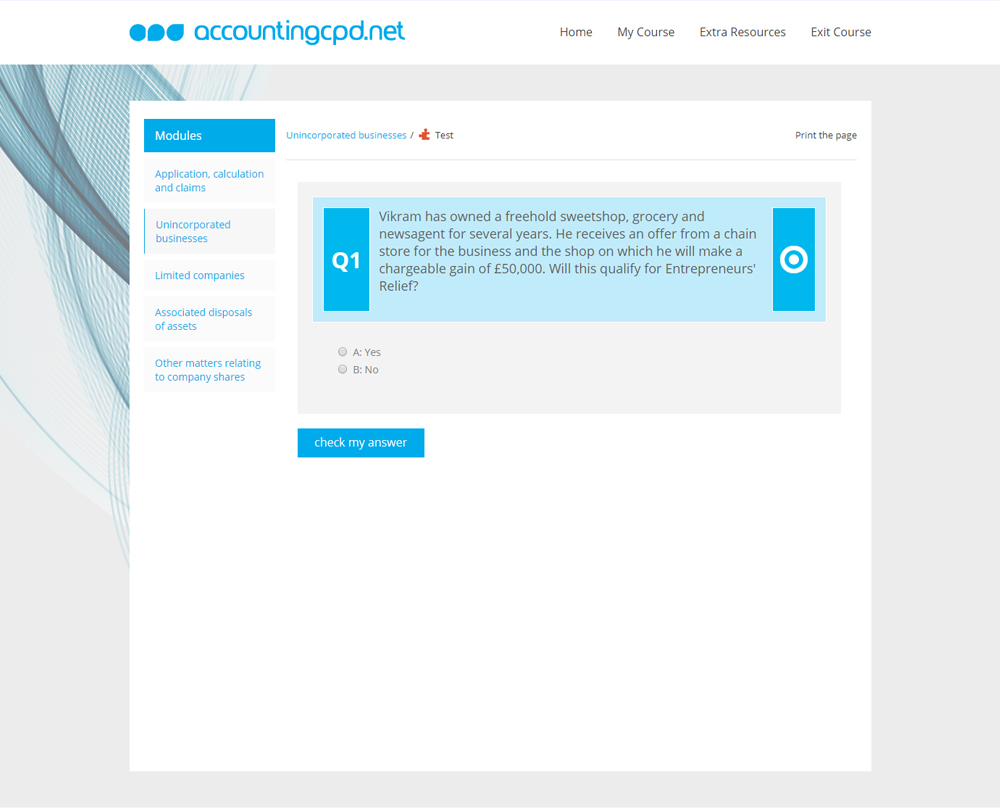

- Unincorporated businesses

- What are the conditions for disposals of unincorporated businesses?

- What constitutes a part of a business?

- What are the conditions for disposals of assets?

- What happens when a business is incorporated?

- Limited companies

- Who are the qualifying shareholders of personal companies?

- What are the qualifying companies?

- What happens with a cessation of trade and the proceeds of liquidation?

- What constitutes a trading company?

- Do EMI share options qualify for relief?

- Associated disposals of assets

- What constitutes a material disposal?

- What counts as withdrawal from the business?

- What assets qualify for relief?

- Where does restricted relief apply?

- How is restricted relief calculated?

- Other matters relating to company shares

- What happens when a qualifying shareholding is diluted by an issue of more shares?

- What happens with exchanges of shares and reorganisations?

- What happens when shares are sold with deferred consideration?

- What relief is available for liquidations?

- Is relief available when selling or liquidating to start again?

- How do we treat gains previously deferred?

How it works

Author

Reviews

You might also like

Take a look at some of our bestselling courses