Try a free course now

Want to see if our CPD works for you? Try a free verifiable CPD course now.

Get started- 48,216 learners

- 133 countries

- 1,500+ CPD resources

- 79% online

Why accountingcpd?

At accountingcpd we help accountants grow by providing high quality CPD, that will genuinely make a difference to you in your career.

Whether you want to keep up to date with the latest changes and trends, develop new skills, or prepare yourself for the next job, accountingcpd has what you need to succeed.

Huge range

Over 1,500 CPD resources to choose from. Keep up to date AND develop your professional skills with courses on a wide range of topics.

CPD Certification

Approved by leading accounting bodies, keep and download your CPD certificates on your personal CPD dashboard. Audit proof and stored securely.

Flexibility

Learn what you want, when and where you want to. From 15-minute CPD Bites, 4-hour courses, to longer-form structured diplomas and qualifications.

Partner approved

We work with leading professional bodies and expert authors to ensure you stay up to date and are able to embrace the future of our profession.

Offers

Courses

2024-25 Update: IFRS

This course covers recent updates to the IFRS reporting framework, including a brand new general standard, a post-implementation review of contract revenue recognition, an Exposure Draft covering financial instruments, and more.

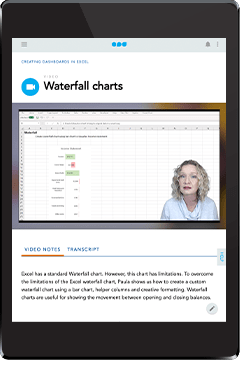

Read more2024-25 Update: Excel

This course covers recent updates and improvements to Excel, including the latest tools to help you handle data, details of formula enhancements, an introduction to the GROUPBY, PIVOTBY, and PERCENTOF functions, as well as some uses for the generative AI powers of Excel’s Copilot.

Read moreIFRS 18: Presentation and Disclosure in Financial Statements

IFRS 18, the first new IFRS since 2017, is going to change the way you work. This course looks in detail at the key elements of this new standard and how it will impact you and the businesses that you work for.

Read moreAI and Ethics

AI is transforming how we work, offering unprecedented efficiency and insights, but also significant ethical challenges. How do we ensure AI operates fairly, transparently, and in alignment with professional standards? Find out how to harness AI responsibly while upholding the integrity and trust central to the accounting profession.

Read more